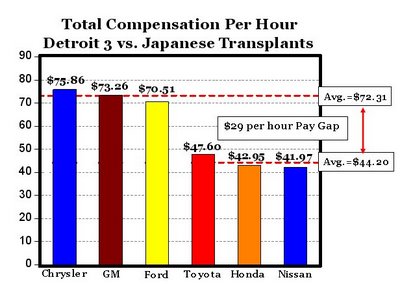

The chart comes by way of Greg Mankiw’s blog

It’s fascinating to watch the auto industry bailout debate unfold. I have a natural aversion to arguments designed to pull at my heart strings, so if I see any version of ‘millions of families’ in the first paragraph, I suspect they are hiding a weak argument and move on. I’ll try to give a flavor of where the argument is today. I have to mention one thing that shocked me. Richard Posner was the first person I respect to use the word depression to describe where he believes we are headed.

Michael Levine in the WSJ – Against:

GM has about 7,000 dealers. Toyota has fewer than 1,500. Honda has about 1,000. These fewer and larger dealers are better able to advertise, stock and service the cars they sell. GM knows it needs fewer brands and dealers, but the dealers are protected from termination by state laws. This makes eliminating them and the brands they sell very expensive. It would cost GM billions of dollars and many years to reduce the number of dealers it has to a number near Toyota’s.

Jeffrey Sachs in the Washington Post – For:

Some want to see the industry punished for its neglect of energy and environmental realities, but we should acknowledge that the SUV era reflected poor judgment across society. Yes, the industry ignored warnings about energy insecurity and climate, but so did the public and politicians. Rather than kill the auto industry, and destroy the U.S. economy in the process, we should fix the industry with a sense of national responsibility and purpose. (We should also fix our ramshackle health-care system, which has burdened the industry and the economy with punitively high costs.)

There are many crucial issues for the design of a long-term restructuring. The government needs the authority to steer a public-private consortium to create a high-mileage-vehicle economy in the coming decade. Public and private funding will be needed for research, development and demonstration of breakthrough technologies. During the restructuring, taxpayers will need protections, including warrants or equity shares, limits on industry compensation, and an equitable restructuring of worker benefits, a process that has already begun because of market hardships.

We face an unprecedented financial calamity, energy crisis and environmental threat. A vibrant, growing U.S. automobile industry should play an essential role in solving all three. The technologies that will win the day are in sight; industry has already made important advances. A partnership with government is vital and should begin this week.

Gary Becker – Against:

Bankruptcy would help GM and Ford become more competitive by abrogating significant parts of their labor contracts with the UAW. One of the greatest needs would be sizable reduction in their health costs through sharp increases in the deductibility and co-payments, and a reduced coverage of medical procedures. Bankruptcy should also help bring the wage rates of GM and Ford in line with those of foreign producers in the US. Some of their pension liabilities may be shifted onto the Pension Benefit Guarantee Corp, but even that would be preferable to an overall bailout.

Judge Posner – For:

The likely psychological impact of a bankruptcy of the U.S.-owned auto industry should not be underestimated. Already consumers, rendered fearful by repeated misinformation from government officials concerning the gravity of the economic situation (including their reluctance to acknowledge that the nation was even in a “recession,” long after it was obvious to the man in the street that we were in something worse), are reducing their buying, precipitating big layoffs in the retail industry, which in turn reduce buying power, which in turn spurs more layoffs. This vicious cycle would be accelerated by the laying off of hundreds of thousands of workers in the automobile industry, including employees of suppliers and dealers as well as of the manufacturers.

All articles referenced are copied in full at end of post.

——————————————————–

Why Bankruptcy Is the Best Option for GM

Chapter 11 would better preserve the valuable parts of the company than an ad hoc bailout.

By MICHAEL E. LEVINE

General Motors is a once-great company caught in a web of relationships designed for another era. It should not be fed while still caught, because that will leave it trapped until we get tired of feeding it. Then it will die. The only possibility of saving it is to take the risk of cutting it free. In other words, GM should be allowed to go bankrupt.

Consider the costs of tackling GM’s problems with some kind of bailout plan. After 42 years of eroding U.S. market share (from 53% to 20%) and countless announcements of “change,” GM still has eight U.S. brands (Cadillac, Saab, Buick, Pontiac, GMC, Saturn, Chevrolet and Hummer). As for its more successful competitors, Toyota (19% market share) has three, and Honda (11%) has two.

GM has about 7,000 dealers. Toyota has fewer than 1,500. Honda has about 1,000. These fewer and larger dealers are better able to advertise, stock and service the cars they sell. GM knows it needs fewer brands and dealers, but the dealers are protected from termination by state laws. This makes eliminating them and the brands they sell very expensive. It would cost GM billions of dollars and many years to reduce the number of dealers it has to a number near Toyota’s.

Foreign-owned manufacturers who build cars with American workers pay wages similar to GM’s. But their expenses for benefits are a fraction of GM’s. GM is contractually required to support thousands of workers in the UAW’s “Jobs Bank” program, which guarantees nearly full wages and benefits for workers who lose their jobs due to automation or plant closure. It supports more retirees than current workers. It owns or leases enormous amounts of property for facilities it’s not using and probably will never use again, and is obliged to support revenue bonds for municipalities that issued them to build these facilities. It has other contractual obligations such as health coverage for union retirees. All of these commitments drain its cash every month. Moreover, GM supports myriad suppliers and supports a huge infrastructure of firms and localities that depend on it. Many of them have contractual claims; they all have moral claims. They all want GM to be more or less what it is.

And therein lies the problem: The cost of terminating dealers is only a fraction of what it would cost to rebuild GM to become a company sized and marketed appropriately for its market share. Contracts would have to be bought out. The company would have to shed many of its fixed obligations. Some obligations will be impossible to cut by voluntary agreement. GM will run out of cash and out of time.

GM’s solution is to ask the federal government for the cash that will allow it to do all of this piece by piece. But much of the cash will be thrown at unproductive commitments. And the sense of urgency that would enable GM to make choices painful to its management, its workers, its retirees, its suppliers and its localities will simply not be there if federal money is available. Like AIG, it will be back for more, and at the same time it will be telling us that it’s doing a great job under difficult circumstances.

Federal law provides a way out of the web: reorganization under Chapter 11 of the bankruptcy code. If GM were told that no assistance would be available without a bankruptcy filing, all options would be put on the table. The web could be cut wherever it needed to be. State protection for dealers would disappear. Labor contracts could be renegotiated. Pension plans could be terminated, with existing pensions turned over to the Pension Benefit Guaranty Corp. (PBGC). Health benefits could be renegotiated. Mortgaged assets could be abandoned, so plants could be closed without being supported as idle hindrances on GM’s viability. GM could be rebuilt as a company that had a chance to make vehicles people want and support itself on revenue. It wouldn’t be easy but, unlike trying to bail out GM as it is, it wouldn’t be impossible.

The social and political costs would be very large, but if GM fails after getting $50 billion or $100 billion in bailout money, it’ll be just as large and there will be less money to soften the blow and even more blame to go around. The PBGC will probably need money to guarantee GM’s pensions for its white- and blue-collar workers (pension support is capped at around $40,000 per year, so that won’t help executives much). Unemployment insurance will have to be extended and offered to many people, perhaps millions if you include dealers, suppliers and communities dependent on GM as it exists now. A GM bankruptcy will make addressing health-care coverage more urgent, which is probably a good thing. It would require job-retraining money and community assistance to affected localities.

But unless we are willing to support GM as it is indefinitely, the downsizing and asset-shedding will have to come anyway. Even if it builds cars as attractive and environmentally responsible as those Honda and Toyota will be building, they won’t be able to carry the weight of GM’s past.

GM CEO Rick Wagoner says “bankruptcy is not an option.” Critics of a bankruptcy say that GM won’t be able to get the loans it will need to guarantee warranties, pay its operating losses while it restructures, and preserve customers’ ability to finance purchases. While consumers buy tickets from bankrupt airlines, electronics from bankrupt retailers, and apartments from bankrupt builders, they say consumers won’t buy cars from a bankrupt auto maker. But bankruptcy no longer means “liquidation” or “out of business” to a generation of consumers used to buying from firms in reorganization.

GM would guarantee warranty support with a segregated fund if necessary. And debtor-in-possession (DIP) financing — loans that provide the near-term cash for reorganizing companies — is very safe, because the DIP lender has priority over all other claimants. In normal markets, it would certainly be available to a GM that has assets to sell, including a viable overseas business. Such financing is probably available even now.

In any event, it would be lined up before a filing, not after, so any problems wouldn’t be a surprise. As a last resort, we could at least consider a public DIP loan to support a reorganizing GM with a good chance to survive — as opposed to subsidizing a GM slowly deflating.

The fate of Daewoo — the Korean auto maker that collapsed in 2000 after filing for bankruptcy, leaving about 500 dealers stranded in the U.S. — is often cited as “proof” that a GM bankruptcy won’t work. But Daewoo was headquartered in a part of the world where bankruptcy still carries a major stigma and usually means liquidation. Daewoo’s experience is largely irrelevant to a major U.S. company undergoing a well-publicized positive transformation, almost certainly under new management.

GM as it is cannot survive without long-term government life support. If it gets that support, it can’t change enough and won’t change fast enough. Contrary to Mr. Wagoner’s brave declaration, bankruptcy is an option. In fact, it’s the only option that merits public support and actually has a chance at succeeding.

Mr. Levine, a former airline executive, is a distinguished research scholar and senior lecturer at NYU School of Law.

———————————————————————————

Gary Becker

Bail Out the Big Three Auto Producers? Not a Good Idea-Becker

The big three American auto producers General Motors, Ford, and Chrysler, are in terrible financial shape. They have asked the government for a bailout, and the Democratic leadership in Congress is eager to give them one. The United Auto Workers union was a strong supporter of President-elect Obama and of Democratic candidates.

These companies have lost tens of billions of dollars during the past few years, and they will shortly run out of cash. GM’s shares have lost almost all their value, and Ford has not done much better. Cerberus Capital, a private equity company, owns Chrysler, and it has lost most of what it invested in the company. For this reason Cerberus is trying get out of the automobile manufacturing business. All three companies were heavily into producing trucks and SUV’s when the sharp run up in gas prices induced consumers to shift away from these gas-guzzlers and toward smaller and more fuel-efficient cars. Moreover, what money GM had been making came mainly not from car production but from its automobile credit business, (GMAC). This company would borrow from banks to lend to consumers who needed help in financing their GM car purchases. The financial crisis has dried up the money available to auto financing companies, and hence eliminated the major source of their profits.

If GM is not bailed out, the company claims it will be forced into bankruptcy within a few months, and Ford’s situation is only slightly better. GM is blitzing Congress, President Bush, and President -elect Obama with pleas for a bailout, followed by a warning that bankruptcy will also hurt auto suppliers throughout the nation that depend on GM’s business. GM is also claiming that bankruptcy will put major financial pressure on the Pension Benefit Guaranty Corp, the federal agency that insures benefits to retirees in the auto industry as well as to million of other workers.

Nevertheless, I believe bankruptcy is better than a bailout for American consumers and taxpayers. The main problem with American auto companies is that during the good times of the 1970s, 1980s and 1990s, they made overly generous settlements with the United Auto workers (UAW) on wages, pensions, and health benefits. Only a couple of years ago, GM was paying $5 billion per year in health benefits to retirees and current employees because their plans had wide health coverage with minimal co-payments and deductibility on health claims by present and retired employees. In those days, the UAW was one of the most powerful unions in the US, and it bargained aggressively with the auto manufacturers, carrying out strikes when its demands were not met. When the American auto industry began to face tough competition from Japanese and German carmakers, they were saddled with excessive pay to their workers, and vastly excessive pensions and health benefits to their current and retired workers.

It is not that cars cannot be produced profitably with American workers: the American plants of Toyota and other Japanese companies, and of German auto manufacturers, have been profitable for many years. The foreign companies have achieved this mainly by setting up their factories in Southern and border states where they could avoid the UAW, and thereby introduce efficient methods of production. Their workers have been paid well but not excessively, and these companies have kept their pension and health obligations under control while still maintaining good morale among their employees. In recent years GM and the other American manufacturers have chipped away at their generous fringe benefits, but their health and retirement benefits still considerably exceed those received by American auto workers employed by foreign companies. As a result of lower costs, better management, and less hindrance from work rules imposed by the UAW, about 1/3 of all cars produced in the US now come from foreign owned plants.

Bankruptcy would help GM and Ford become more competitive by abrogating significant parts of their labor contracts with the UAW. One of the greatest needs would be sizable reduction in their health costs through sharp increases in the deductibility and co-payments, and a reduced coverage of medical procedures. Bankruptcy should also help bring the wage rates of GM and Ford in line with those of foreign producers in the US. Some of their pension liabilities may be shifted onto the Pension Benefit Guarantee Corp, but even that would be preferable to an overall bailout.

A good analogy is what happened to United Airlines. By entering bankruptcy it was able to reduce its inflated cost structure by breaking contracts it had with the pilots union and other employee unions. It exited bankruptcy a slimmer and more efficient airline. Whether it is able to compete effectively in the long run is still not certain, but it is in much better shape to compete than before it entered bankruptcy.

Bankruptcy may also force out the current management of GM and Ford. I do not know for certain whether they have competent management- GM surely did not have top management for much of its recent history. I do believe, however, that when a coach of a team loses a few games, he might legitimately explain that by injuries, bad luck, or even bad officiating. These excuses become lame when he consistently loses many games, and the correct and common practice is then to fire the coach. The same considerations apply to top management. When a company consistently does badly while some of its competitors (like Toyota) are doing well, its time to fire the management team, and see if another team can do better.

Is GM “too big” to fail? I do not believe the company is too big to go into a reorganization-which is what bankruptcy would involve. Such reorganization would abrogate its untenable labor contracts, and give it a chance to survive in long run. A bailout, by contrast, would simply postpone the needed reforms in these labor contracts, the business model of GM, and its management.

Posted by becker at 08:34 PM | Comments (13) | TrackBack (0)

————————————————-

Richard Posner

Bail Out the Detroit Auto Manufacturers? Posner’s Comment

Becker has laid out the case for refusing to bail out GM, Ford, and Chrysler. It is a powerful case, and if the drop in auto sales that is driving these companies toward insolvency had occurred two years ago, there would be in my view no case, other than a political one, for a bailout. But in the current financial crisis, I believe a bailout is warranted, provided that the shareholders and managers of the companies are not allowed to profit from it.

There are two types of corporate bankruptcy: liquidation and reorganization (Chapter 7 and Chapter 11 of the Bankruptcy Code, respectively). In a liquidation the bankrupt company closes down, lays off all its workers, and sells all its assets. That probably would not be the efficient solution to the problems of the Detroit automakers. They are still producing millions of motor vehicles per year, and if they suddenly ceased production entirely there would be a big shortage even though demand is way down. To put this another way, although at present the companies are probably losing money on virtually every vehicle they sell, at a lower level of production the price at which they sold their vehicles would exceed marginal cost.

The alternative to liquidation–reorganization–can work well in normal times, as in the United Air Lines bankruptcy that Becker mentions. The reorganized business is able to borrow money because its post-bankruptcy borrowings (“debtor in possession” loans, as they are called) are given priority over its pre-bankruptcy debts, which are usually written down in bankruptcy, reducing the reorganized firm’s debt costs and thereby enabling it to recover solvency. The debts that get written down can include health and pension benefits, which in the case of the auto companies continue to be a big drag on profitability.

The major problems with allowing the automakers to be forced into bankruptcy within the next few months are three, all arising from the depression that the nation appears to be rapidly sinking into. The first problem is that the companies might have to liquidate, because they might be unable to attract the substantial post-bankruptcy loans that they would need to enable them to remain in business. The credit crunch–less politely the near insolvency of much of the banking industry–has made that industry unable or unwilling to make risky loans, and loans to the auto companies after they declared bankruptcy would be risky.

Second, not only the size of the automakers, but peculiarities of the industry, would cause bankruptcy to greatly exacerbate the nation’s already dire economic condition. In the very short term, the automakers would probably stop paying their suppliers, which would precipitate a number of the latter–already in perilous straits because of the plunge in the number of motor vehicles being produced–into bankruptcy. Many of the suppliers would probably liquidate, generating many layoffs. At the other end of the supply-distribution chain, consumers would be reluctant to buy cars or other motor vehicles manufactured by a bankrupt company because they would worry that the manufacturer’s warranties would be unenforceable. So more dealerships would close, producing more bankruptcies, liquidations, and layoffs. With the demand for the vehicles made by the Detroit automakers further depressed and the supply-distribution chain in disarray, the liquidation of those companies would begin to loom as a real and imminent possibility. Liquidation of the automakers would produce an enormous number of layoffs up and down the chain of supply and distribution. Such prospects reinforce the unlikelihood that a reorganized industry could survive on debtor in possession loans.

The likely psychological impact of a bankruptcy of the U.S.-owned auto industry should not be underestimated. Already consumers, rendered fearful by repeated misinformation from government officials concerning the gravity of the economic situation (including their reluctance to acknowledge that the nation was even in a “recession,” long after it was obvious to the man in the street that we were in something worse), are reducing their buying, precipitating big layoffs in the retail industry, which in turn reduce buying power, which in turn spurs more layoffs. This vicious cycle would be accelerated by the laying off of hundreds of thousands of workers in the automobile industry, including employees of suppliers and dealers as well as of the manufacturers.

The U.S.-owned auto industry may be doomed; it may simply be unable to compete with foreign manufacturers (including foreign manufacturers that have factories in the U.S.); or a reorganization in bankruptcy may be the industry’s eventual salvation. But the automakers should be kept out of the bankruptcy court until the depression bottoms out and the economy begins to grow again. (Recall that the government bailed out the airlines after 9/11, allowing United Air Lines to have an orderly bankruptcy reorganization beginning the following year and ending in 2006.) Any bailout, however, should come with strict conditions, to minimize the inevitable moral hazard effects of government bailouts of sick companies. The government should insist on being compensated by receipt of preferred stock in the companies, on the companies’ ceasing to pay dividends, and on caps on executive compensation, including severance pay.

A possible alternative would be for the government to refuse to bail out the industry but agree to provide the necessary debtor in possession loans to keep the auto companies from liquidating after they declare bankruptcy. But this would be a kind of bailout, and probably would not be sufficient to avert the shock effects that I have described.

Posted by Richard Posner at 06:59 PM | Comments (18) | TrackBack (0)

—————————————————————————–

Jeffrey Sachs

A Bridge for the Carmakers

The Future Is in Sight. They Just Need Help Getting There.

By Jeffrey D. Sachs

Monday, November 17, 2008; A19

A government-supported restructuring of the auto industry is urgently needed for our economic and energy security. If the Bush administration allows the auto industry to collapse, it will compound the panic that started with the bankruptcy of Lehman Brothers. Washington should seize the opportunity to begin a new era of U.S. technological leadership in the global auto industry, starting with an immediate loan.

First, this is an opportunity to embark on a major industry restructuring to position the United States to lead the world in producing cars that get 100 miles or more per gallon. This achievement is closer than many suppose, with the pathbreaking plug-in hybrid Chevy Volt set to arrive in 2010 and several new hybrid models on the way. American-made fuel-cell cars may be a large-scale reality within a decade. Success would dramatically improve energy and national security, climate security, and U.S. global competitiveness, and a public-private partnership is needed to bring about this transformation.

Second, the sudden closure of an automaker would be catastrophic, possibly pushing our economy from recession to depression. Because of the impact on parts suppliers, the shutdown of one company would imperil domestic production across the board, and the jobs at risk include not only the 1 million in vehicle assembly and parts but millions more that would be caught in the resulting cascade of failures. The industrial Midwest — especially Michigan, Ohio, Indiana, Illinois and Tennessee — would be devastated, and the shock waves would reverberate across the world.

Third, any restructuring under Chapter 11 bankruptcy rules would be a death knell. Yes, in some industries, Chapter 11 can provide breathing space. For the automakers, however, it would accelerate the collapse of consumer demand and the mass bankruptcy of parts manufacturers. Consumers choose vehicles in part on their expectation of the long-term health of the companies that make them, which they rely on for parts, service and resale values.

The industry does not need a shakeout but a change of technology for long-term energy and climate security. The recent collapse of annual sales, from 17 million vehicles to 11 million, is not permanent but cyclical. Over time, sales will increase, especially as people in China, India and other emerging markets become buyers. A forecast of U.S. sales of 15 million to 20 million units a year is justified by normal replacements among the 240 million passenger vehicles Americans now own, and the U.S. market will also grow along with population and income.

Yet the automakers cannot turn to ordinary borrowing to tide them over until that happens because of the ravaged capital markets. The risk spreads of corporate bonds over U.S. Treasuries are the highest ever, and many borrowers can’t get credit at any price. That’s why the government has embarked on nearly $1 trillion in direct interventions. A small part of that should be used for the auto industry.

In this environment, the normal market test of consumer demand can’t be used to judge which industries should survive. We are experiencing the steepest temporary decline in consumer spending since the Depression. Consumer financing for autos has collapsed. Households are retrenching after the greatest wealth loss in equities and housing in history.

And a transformation of the type that’s required for long-term sustainability of the automakers will require both the market and government. Public policies and funding are needed to support the research and development of high-performance batteries and fuel cells and, especially, to modernize the national power grid and other infrastructure. These are steps that individual auto companies (and even the industry as a whole) could not accomplish on their own.

Some want to see the industry punished for its neglect of energy and environmental realities, but we should acknowledge that the SUV era reflected poor judgment across society. Yes, the industry ignored warnings about energy insecurity and climate, but so did the public and politicians. Rather than kill the auto industry, and destroy the U.S. economy in the process, we should fix the industry with a sense of national responsibility and purpose. (We should also fix our ramshackle health-care system, which has burdened the industry and the economy with punitively high costs.)

There are many crucial issues for the design of a long-term restructuring. The government needs the authority to steer a public-private consortium to create a high-mileage-vehicle economy in the coming decade. Public and private funding will be needed for research, development and demonstration of breakthrough technologies. During the restructuring, taxpayers will need protections, including warrants or equity shares, limits on industry compensation, and an equitable restructuring of worker benefits, a process that has already begun because of market hardships.

We face an unprecedented financial calamity, energy crisis and environmental threat. A vibrant, growing U.S. automobile industry should play an essential role in solving all three. The technologies that will win the day are in sight; industry has already made important advances. A partnership with government is vital and should begin this week.

Jeffrey D. Sachs is director of the Earth Institute at Columbia University and the author of “Common Wealth: Economics for a Crowded Planet.”

————————————————-